Apr 09, 2026

Helium Shortage Update: April 9, 2026

While much of the economic discourse around the US-Israeli war on Iran concerns the constraints t...

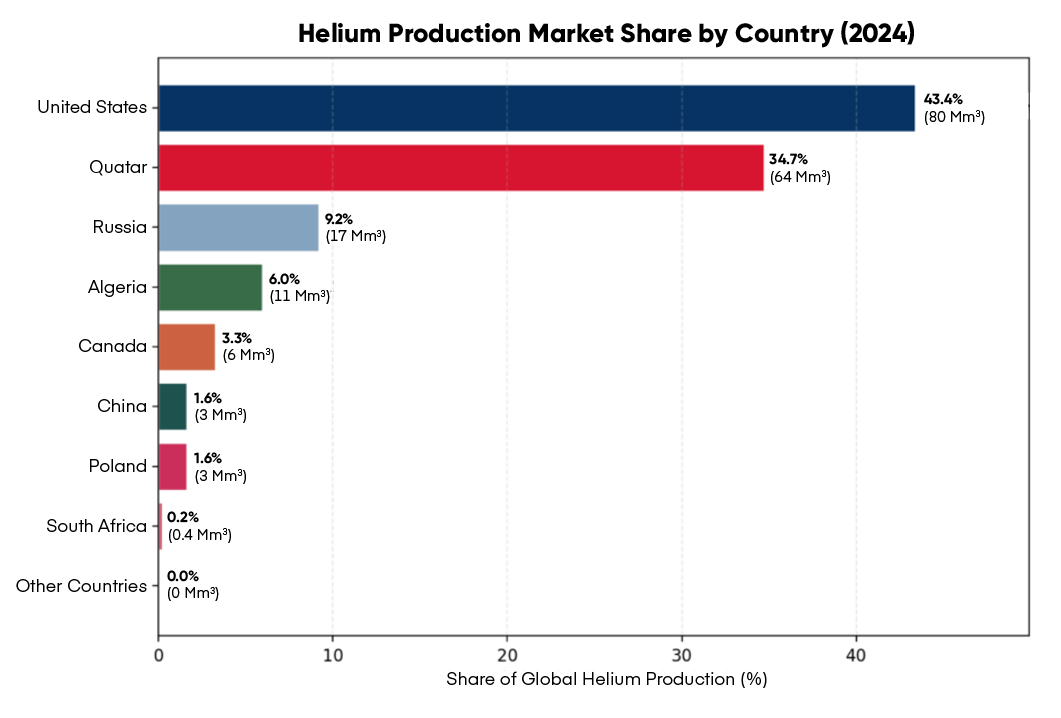

While much of the economic discourse around the US-Israeli war on Iran concerns the constraints to oil production, which is affecting manufacturing, logistics, and costs of goods around the world, a secondary risk is the effect on helium availability. Qatar, which sits on the opposite side of the Persian Gulf from Iran, supplies approximately 35 percent of the helium on the global market, and semiconductor manufacturers—especially companies in Taiwan and South Korea—use a significant percentage of the extracted helium in their production processes.

Helium is a hidden chokepoint in the semiconductor-manufacturing supply chain, and there are no real substitutes for its main use. Although some other gases can be used in specific cases, losing a critical supply of helium can shut down an entire line.

The concern doesn’t come from the effects of the missing Iranian supply of oil, natural gas, and helium, but rather from the danger to shipping lanes within the Strait of Hormuz and the possible stranglehold that has on exports from Qatar. The only way for it to supply its customers is through the strait, as there are no secondary logistic lines for natural-gas by-products such as helium. The ongoing conflict is still tumultuous, with restrictions changing on a minute-to-minute basis. Given the uncertainty, semiconductor manufacturers have been placed in a difficult position.

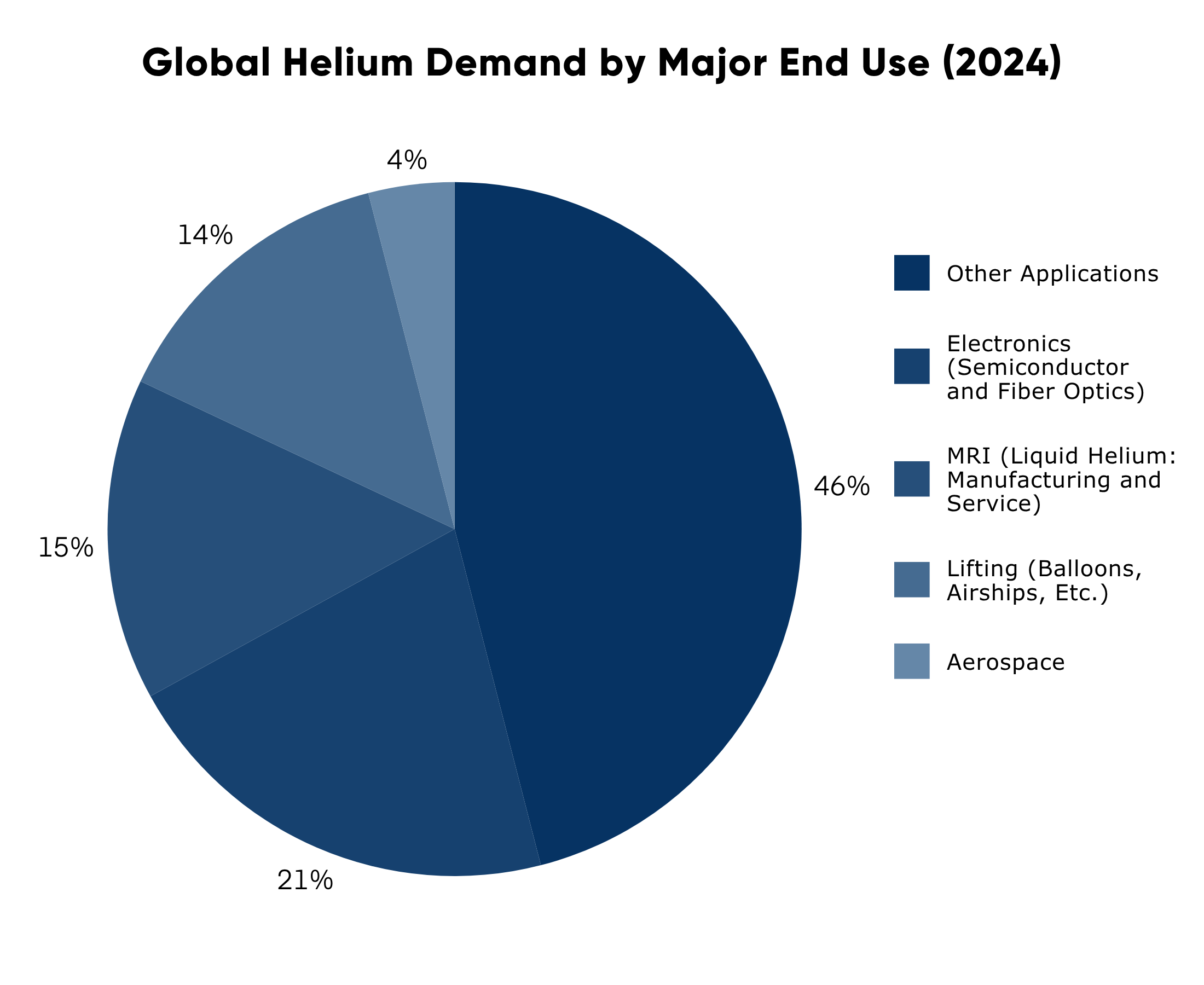

The semiconductor industry is the largest user of helium, accounting for 20 to 25 percent of the world’s annual helium consumption. That market share is projected to be 30 percent by 2030.

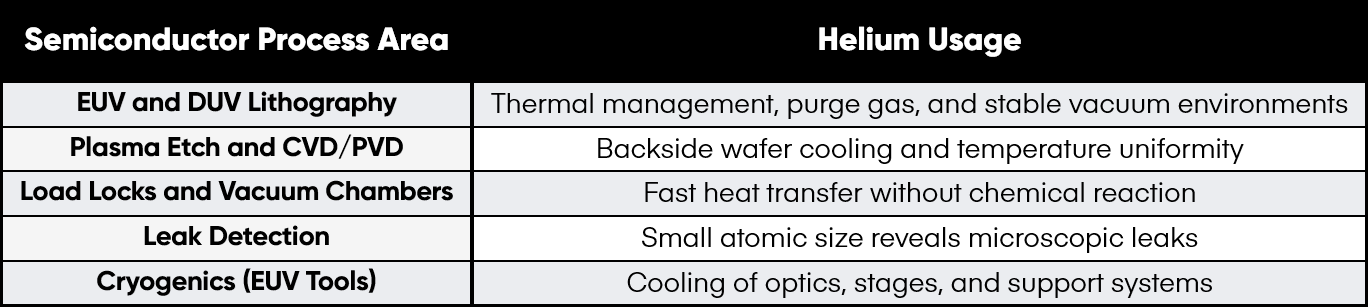

The reason for that expected growth is that most of its use is in the EUV and UV lithography stage of advanced logic production. With the vast data center expansions and the continued need for computing power in consumer and embedded electronics, this is the most crucial and fastest-growing semiconductor segment. DRAM, HBM, NAND, GPUs, CPUs, high-performance analog products, MCUs for advanced electronics, and more all require this type of lithography.

Most leading-edge fabs reclaim 70 to 95 percent of helium, especially in EUV tools, depending on the age and class of the machine. This strategy was explored decades ago when chip manufacturers began to understand the various vulnerabilities within their supply chains.

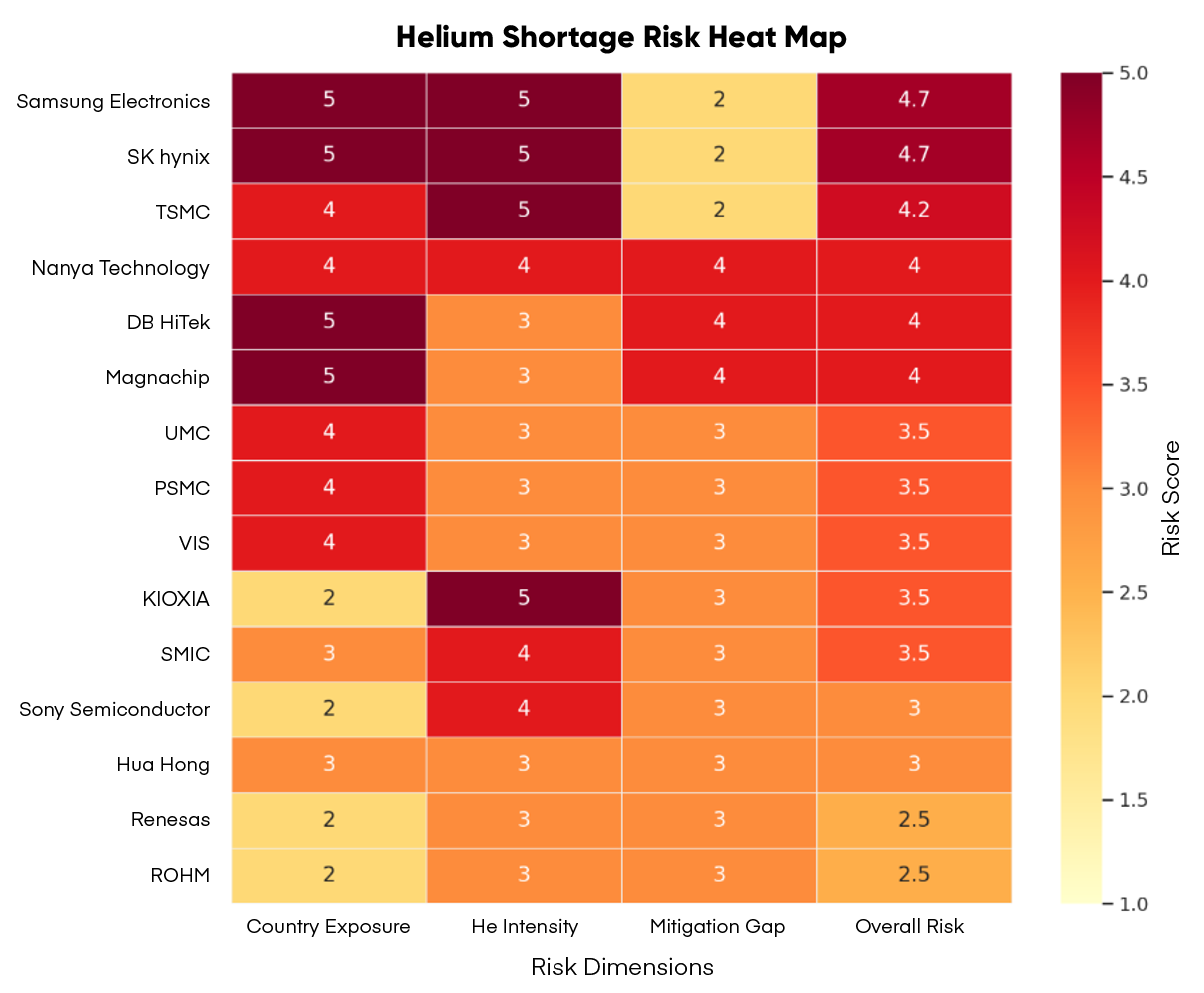

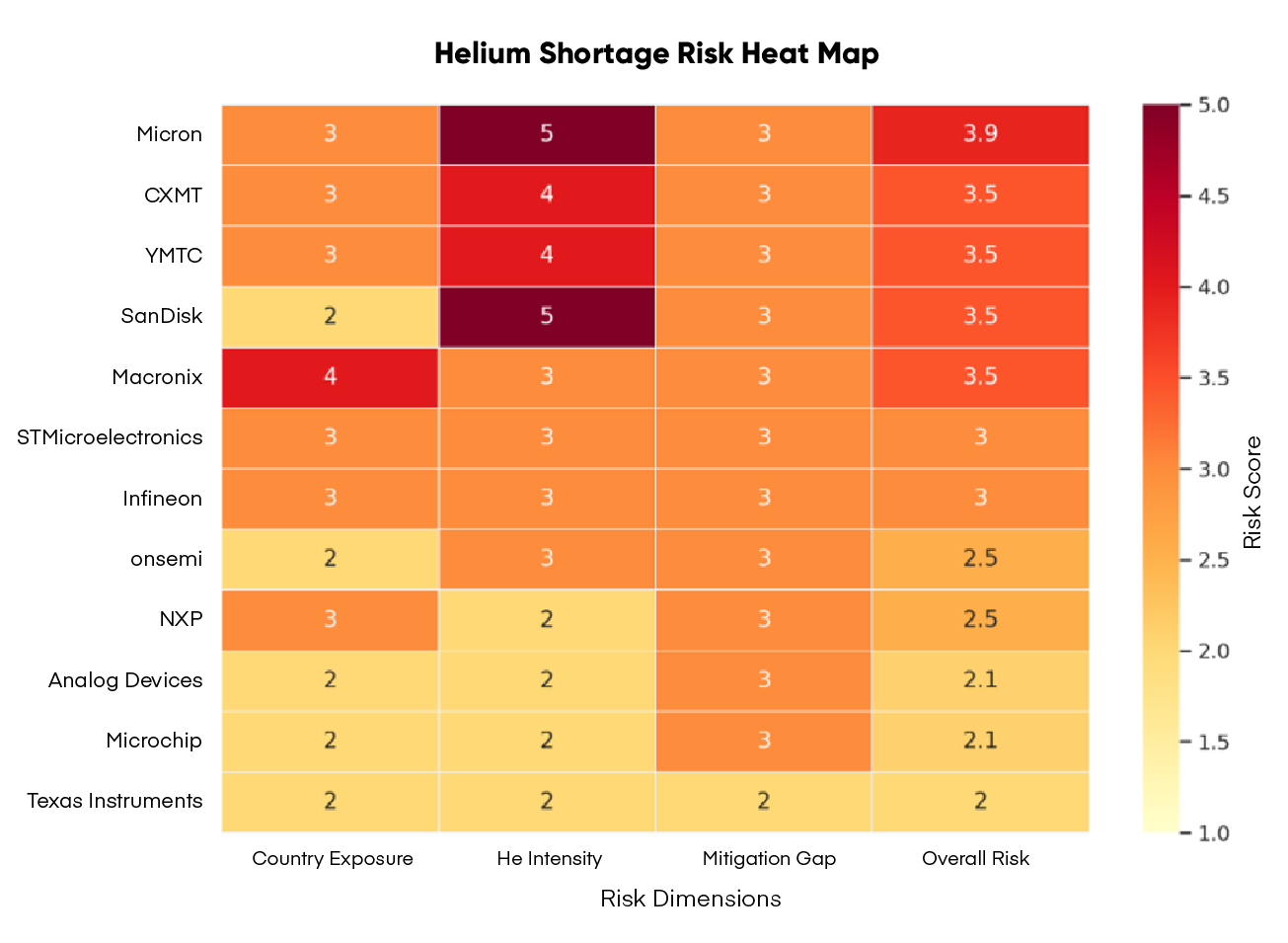

The main focus of industry worries surrounds major Taiwanese and South Korean suppliers, which are more dependent on helium from Qatar than Japanese and US fabs. TSMC, PSMC, VIS, Samsung, and SK hynix are major users, but all foundries that create advanced logic ICs are exposed to risk.

The amount of buffer inventory at fabs varies greatly throughout the industry, with the major players ranging from under one month to six months of coverage.

Thus far, most users have stated that they have sufficient inventory to produce without interruption and will work to realign their suppliers. Most of them also depend upon their suppliers to have buffer inventory on hand. Currently, a shutdown of the strait for 60 to 90 days would start causing possible constraints on semiconductor manufacturers.

Should that 60- to 90-day timeframe approach, helium constraints are likely to affect smaller industries first, allowing the semiconductor industry to work normally. This is due to the importance of semiconductors in today’s society, their total market share, and users’ willingness and ability to pay higher prices for product. If semiconductor makers do begin to lose supply, then each will have to reallocate manufacturing, likely emphasizing AI demand over others.

Despite the risk to the helium supply, those most exposed have informally stated they have sufficient supply on hand and with vendors to navigate the possible instability without interruption.

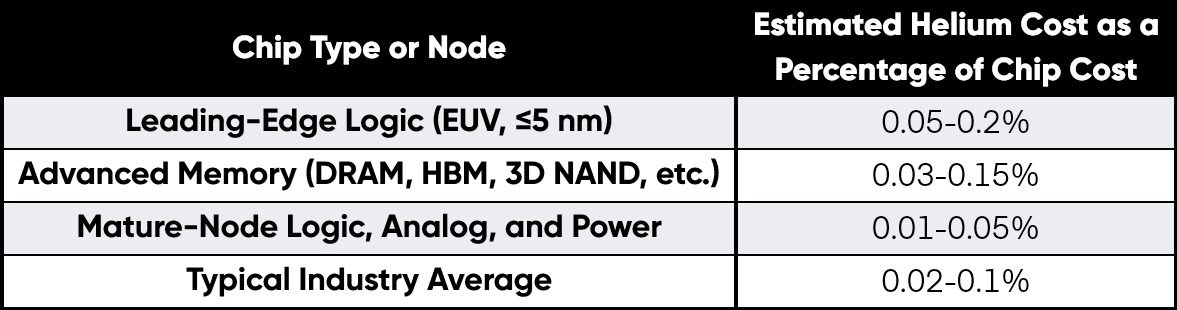

Costs for helium increased rapidly due to the suddenness of the conflict, despite global supply stability in the short term. However, despite its large market share, helium costs have a relatively small effect on semiconductor production costs. For example, an EUV logic wafer costs USD $18,000, while helium related to its production only costs USD $6.

Thus far, semiconductor makers have not noted price increases due to helium prices specifically, though many have been increasing prices due to a wide range of upstream inflationary costs.

Smith’s team of experts brings a diverse wealth of knowledge and experience that helps us offer the most relevant and actionable insights into the global electronic-component marketplace. As geopolitical disruptions continue to affect the semiconductor industry, follow Smith’s Market Blog to stay up to date on the latest information.

We will continue to monitor the situation and share the latest updates as they become available.

Helium Shortage Update: April 9, 2026

While much of the economic discourse around the US-Israeli war on Iran concerns the constraints t...

Smith Will Exhibit at Microelectronics US 2026, Booth 616

The company will showcase its scalable supply chain solutions and commitment to quality at the Mi...

Smith Opens New Sales Office in Boston

The new location will foster deep connections and drive innovation with both new and existing par...

您可通过以下三种方式,轻松关注Smith微信公众号: